CPI cooled, jobs surged. So why is the market pricing a recession?

Because rising oil and geopolitical risk are changing the story.

It is now mid-April, and the market is still stuck in uncertainty.

US–Iran talks continue to swing between optimism and disappointment. At the same time, two of the most important data points have just been released:

- CPI came in below expectations

- Nonfarm payrolls came in far above expectations

Two signals.

Two different directions.

Under normal conditions, that combination would support risk assets. But with oil prices rising and geopolitical tensions escalating, markets are no longer focused on growth they are starting to price in recession risk.

So what is the market actually telling us?

In this piece, we break down:

- What the March CPI really means

- Why strong jobs data may not be bullish

- And where markets could be heading next

1. CPI Shock: Lower Than Expected, But Not Comforting

When the March CPI was released, markets reacted instantly.

At the #DooTrader Trading World Cup in Bali, rankings shifted sharply the moment the data hit.

If you went long gold at that moment, you likely captured the move.

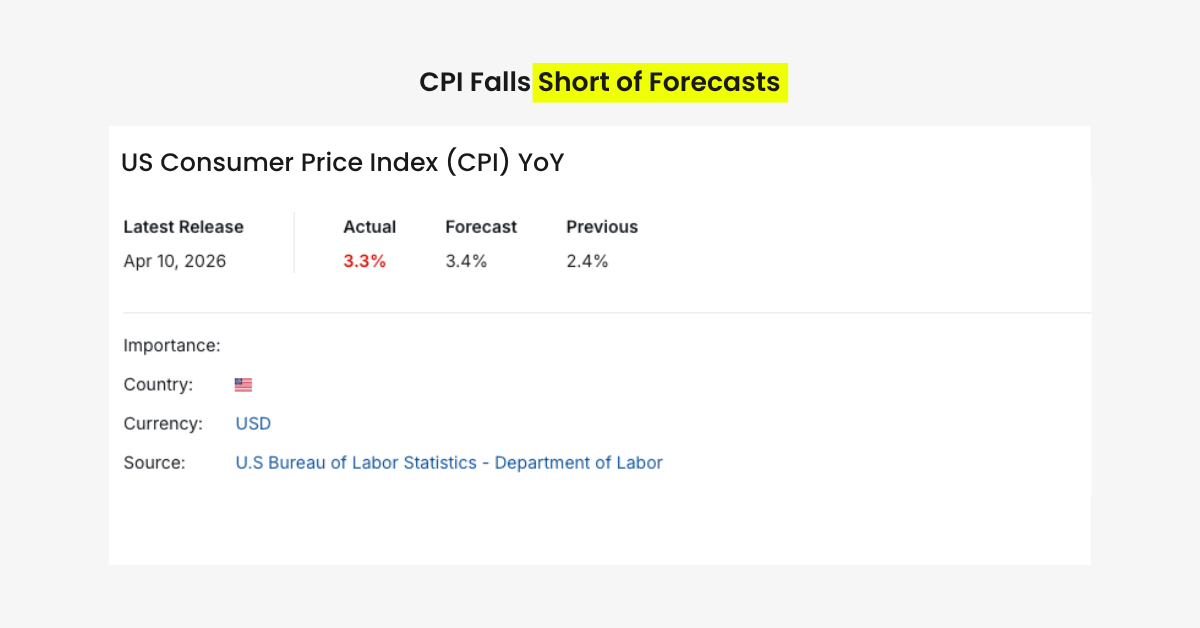

Because the US Consumer Price Index (CPI) came in below expectations.

The Headline Looks Good But Look Deeper

- Previous CPI: 2.4%

- Expected: 3.4%

- Actual: 3.3%

At first glance, this looks like a positive surprise.

And markets reacted accordingly:

- Gold surged

- Oil pulled back

But the bigger story is not the headline.

It is what’s driving it.

Energy Is Back in Control

Energy prices surged:

- +12.5% YoY

- Up 12 percentage points from February

That is a sharp acceleration.

Meanwhile:

- Food inflation eased slightly to 2.7%

- Housing remained stable at ~3%

This tells us one thing:

Energy is now the dominant driver of inflation

Why This Matters for the Fed

Without the US–Iran conflict, inflation would likely be under control.

Rate cuts would be more certain.

But now, everything depends on oil.

And oil depends on geopolitics.

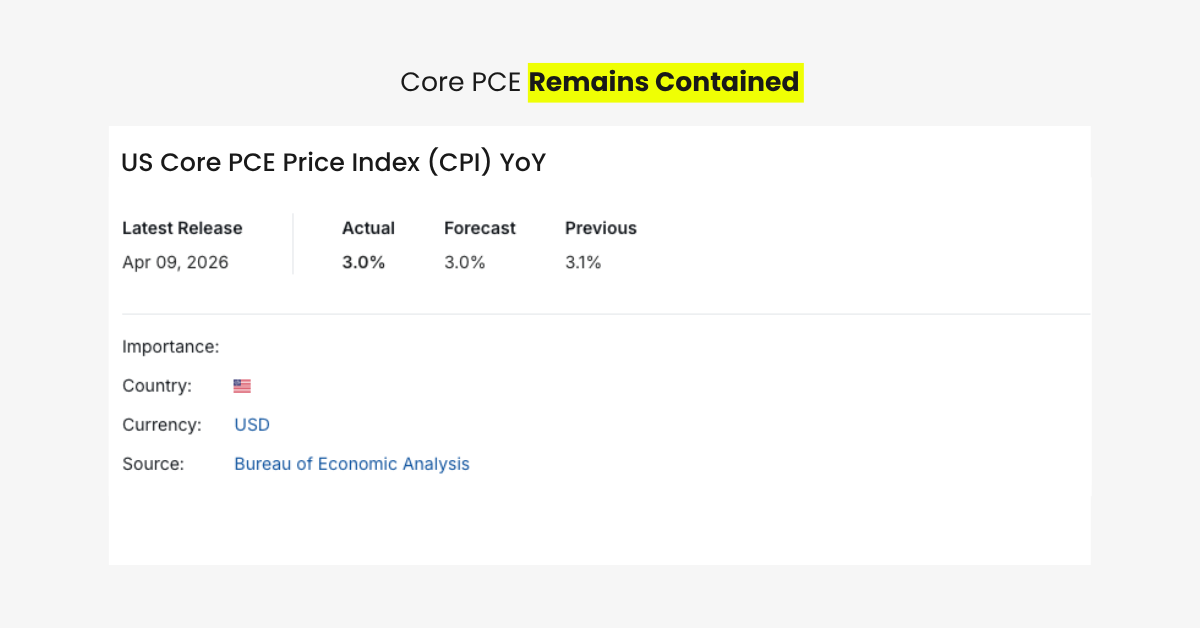

The Only Good News: Core Inflation Is Stable

Strip out food and energy:

- Core CPI: 3.0%

- Slightly below the previous 3.1%

This reduces the risk of a major inflation shock.

But it does not remove the risk entirely.

Because if oil stays high, inflation can still come back.

2. Strong Jobs But Not Bullish

Now comes the second surprise.

The labor market.

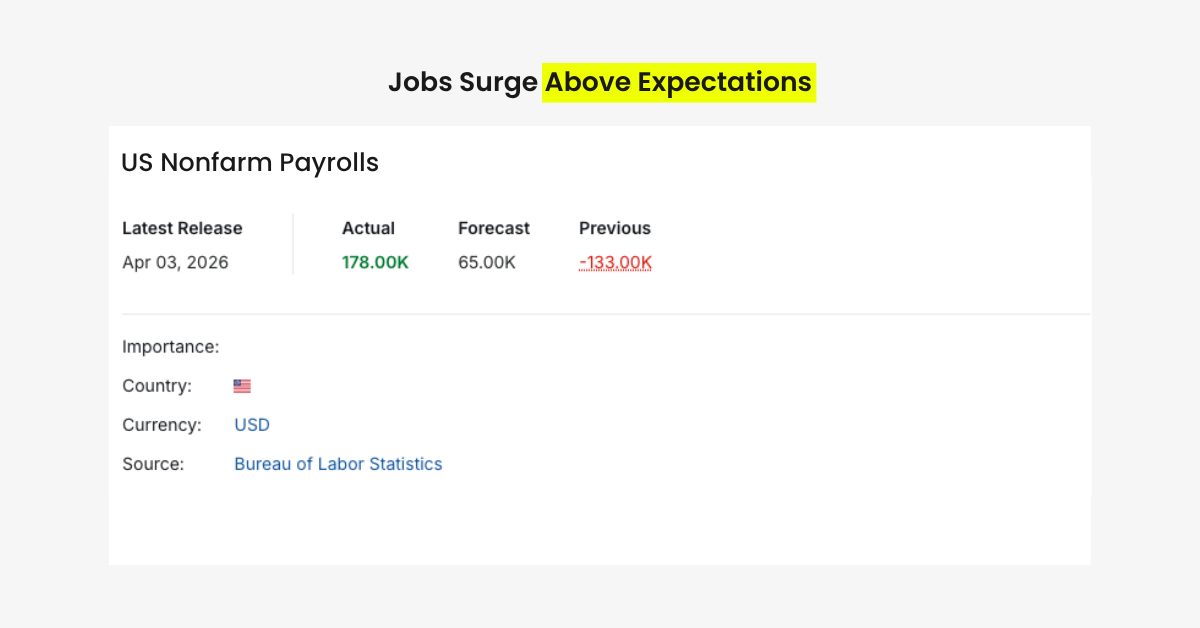

The Headline: Stronger Than Expected

- Jobs added: 178,000

- Expected: 60,000

- Unemployment: 4.3%

On paper, this looks strong.

But markets did not celebrate.

Why?

Strong Jobs = Fewer Rate Cuts

In this environment, strong data is not always good.

Because:

- Strong jobs reduce the need for rate cuts

- Rising oil increases inflation risk

Together, they create a problem:

The Fed has less reason to ease

Some investors are even asking:

Could rate hikes come back into the conversation?

Observation on the Market: Don’t Overreact

This jobs number may not be as strong as it looks.

It was boosted by:

- strike resolutions

- seasonal hiring (spring effect)

At the same time:

- JOLTS job openings have fallen to 4.2%

- Small business optimism is weakening

This suggests the labor market is:

Stable in the short term

Softening in the long term

The Real Twist

In today’s market:

Weaker data is not bad

Because it reduces the risk of further tightening.

That is the paradox.

3. The Real Shift: From Inflation to Recession

This is where things get interesting.

The market is no longer just trading inflation.

It is starting to price recession risk.

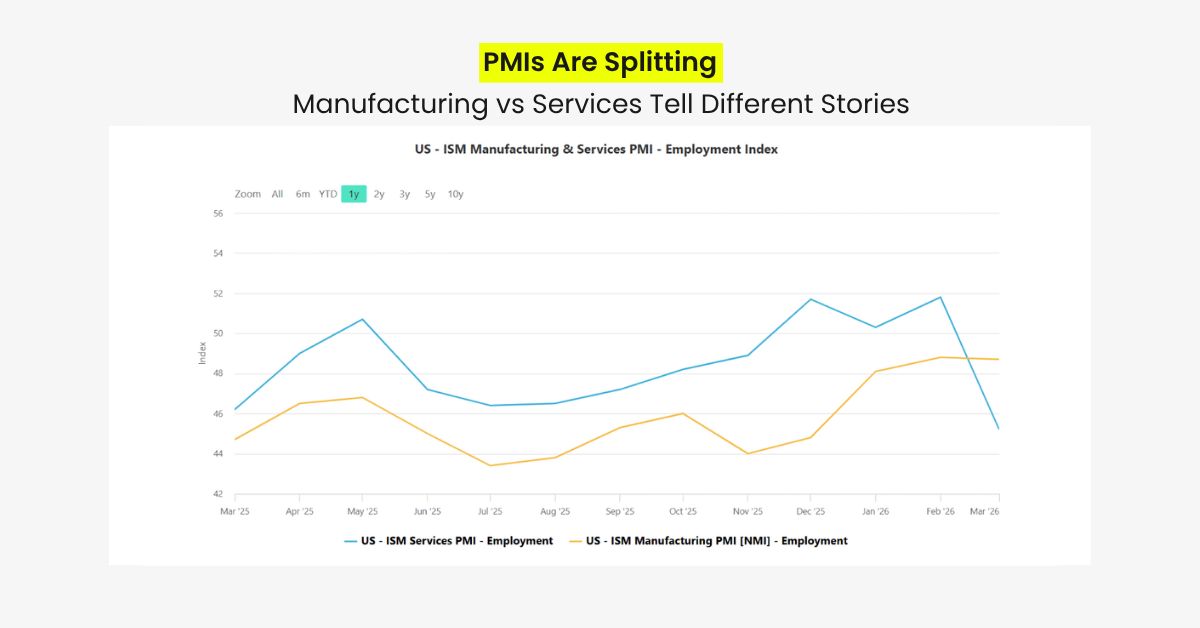

The PMI Signal

On the surface, PMI looks stable.

But underneath, the story is changing.

- Manufacturing PMI: 48.7

- Services PMI: dropped from 51.8 → 45.2

That is a sharp decline.

Why This Matters

Manufacturing may be supported by:

- inventory buildup

- war-related demand

But services tell the real story.

And right now:

Services are weakening

Fear vs Reality

The market’s concern about recession is justified.

But it may also be overreacting.

Geopolitics is amplifying fear.

4. What Comes Next: Panic, Recovery, Repeat

Based on D Prime’s observation:

Markets are entering a cycle of:

panic → recovery → panic → recovery

And this pattern may continue in the near term.

The Core Conflict Is Deeper Than Oil

At the center of the US–Iran tension is not just energy.

It is policy.

- The US wants limits on Iran’s nuclear program and regional influence

- Iran demands sovereignty and reduced US presence

These are fundamental disagreements.

And they are not easy to resolve.

But the Market Is Adapting

Monday’s price action revealed something important.

Over the weekend:

- Panic surged

- Crypto dropped sharply

But by market open:

- Sentiment stabilized

- Stocks and gold both closed higher

This tells us:

War risk is no longer a surprise

And That Changes Everything

After nearly two months, markets are adjusting.

- Conflict is priced in

- Inflation is expected

- Recession risk is understood

And when everything is priced in…

What This Means for Markets

It often signals a turning point.

Not certainty.

But opportunity.

A Shift in the Narrative

The market is no longer reacting.

It is adapting.

And that is a critical difference.

Because once fear becomes familiar, it loses power.

And when fear is priced in:

The bottom often forms quietly

Before the news improves